The Board of Jubilant Ingrevia Limited met today to approve financial results for the quarter ended March 31st, 2026.

Commenting on the Company’s performance, Mr. Shyam S Bhartia, Chairman and Mr. Hari S Bhartia, Co- Chairman, Jubilant Ingrevia Limited said:

“We are pleased to report a healthy performance in Q4 and FY26. Our Revenue grew 12% YoY and EBITDA increased 11% YoY in Q4 FY26, reflecting our strong execution. A key highlight for the quarter was our effective handling of the Middle East crisis, with no force majeure and zero production loss. The other highlights include

successful dispatch from our newly constructed Agro CDMO facility and the

acquisition of Remidex to accelerate the growth of our Human Nutrition business.

The Board has recommended a final dividend of Rs.2.50 per share (250%), taking total FY26 dividend to Rs.5 per share (500%)

Overall chemical Industry’s demand remains resilient despite Middle East disruptions. Volumes continue to grow, while pricing has firmed up in last few weeks due to higher crude-linked costs, with effective pass-through to customers.

Pharmaceuticals continue to anchor growth with strong volumes and consistent demand.

Agrochem saw strong growth, with robust export visibility and successful price increases, especially in second half of the quarter.

Nutrition and Personal Care markets witnessed volume and price-led growth, driven by Niacinamide, with strong demand in Feed and Cosmetics.

Future Outlook:

Early outcomes of our Pinnacle journey are clearly visible in our performance, with strong EBITDA growth, an improving portfolio mix, enhanced customer relationships, a robust opportunity pipeline, more efficient cost structure and balance sheet. With improving volume demand and escalated pricing, we are confident of sustained growth going forward across our segments.

For FY27, we expect growth to be led by Specialty Chemicals and Nutrition, along with recovery in Acetyls. We are expecting a sequential growth in revenue and EBITDA in coming quarters, starting with Q1FY27 itself.

We will continue to invest further in the business; the construction of Gajraula Multi Purpose Plant (MPP) is progressing well, this will further strengthen our CDMO growth roadmap.”

Commenting on the Company’s performance, Mr. Deepak Jain, Chief Executive Officer and Managing Director, Jubilant Ingrevia Limited said:

“Over the past year, we have made strong progress across all strategic pillars, building long-term growth while managing global challenges effectively. Despite Middle East disruptions impacting supply and prices, our diversified sourcing and agility ensured minimal disruption with effective cost pass-through.

Strong customer engagement and timely renegotiations have strengthened resilience, reflected in improved performance in Q4.”

Let me share the overall Business update with you all:

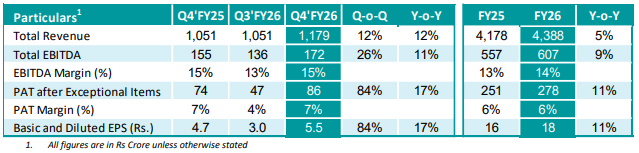

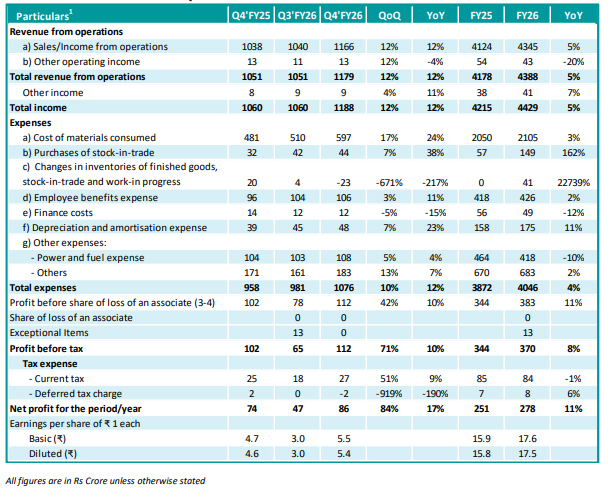

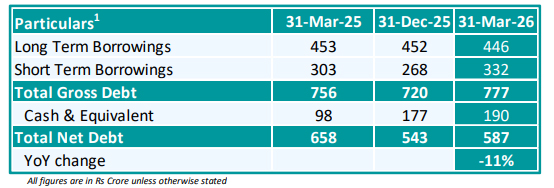

1) Q4 recorded highest revenue in 14 quarters at Rs.1,179 crore, up 12% YoY, driven by 10% volume growth. EBITDA stood at Rs.172 crore, up 11% YoY and 26% QoQ. PAT was ?86 crore, up 17% YoY and 84% QoQ. Net debt/EBITDA improved to 0.99x. Our net debt has reduced by 11% in 2026

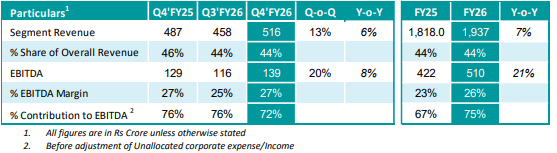

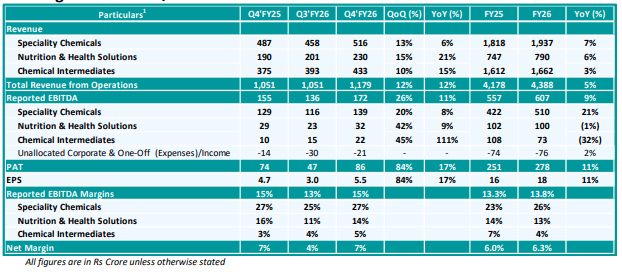

2) In Our Speciality Chemical Business, Revenue stood at Rs.516 crore rose +6% YoY and 13% QoQ. EBITDA stood at Rs.139 crore; with margins at ~27%.

a) FY26 revenue stood at Rs.1,937 crore up +7%, EBITDA stood at Rs.510 crore up 21%.

b) During the quarter, Specialty Chemicals showed strong momentum, driven by volume recovery despite stable pricing, with margins rising above 27%, reflecting robust fundamentals and resilience.

c) Our Pyridine & derivatives showed strong volume growth.

d) Our Fine Chemicals & Diketene derivatives recorded steady QoQ and strong YoY growth.

e) Our CDMO business progressed well with higher realizations and commencement of a large Agro contract, reflecting a shift towards value-added products.

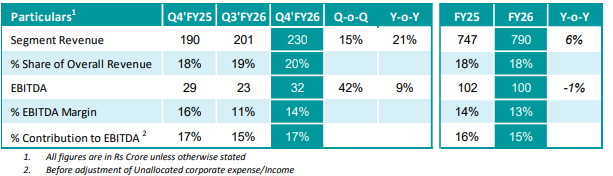

3) In our Nutrition & Health Solutions Business Segment, Revenue stood at Rs.230 crore up 21% YoY and 15% QoQ. Segments EBITDA stood at Rs.32 crore up by 42% QoQ and margins stood at 14%.

a) FY26 revenue stood at Rs.790 crore and EBITDA at Rs.100 crore.

b) We witnessed a strong recovery during the quarter, with growth driven predominantly by volumes across segments.

c) Growth was led by Niacinamide, supported by Cosmetics demand; Choline also improved with a surge in exports to Europe

d) We completed the acquisition of Remidex Pharma, expanding presence in human nutrition and premix solutions.

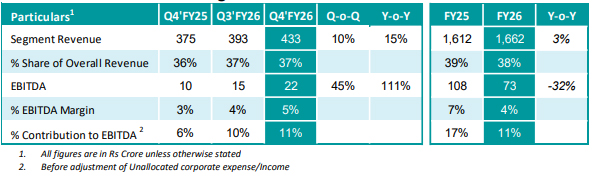

4) In our Chemical Intermediate Business Segment, Revenue stood at Rs.433 crore, up 15% YoY and 10% QoQ.

Segments EBITDA improvement supported by cost pass-through. In our Chemical Intermediates business, domestic volumes improved on the back of stronger agrochemical and paracetamol demand. We remain optimistic about recovery, supported by European force majeure events and plant closures. While Middle East disruptions firmed input costs, rising acetic acid prices have set the stage for a favorable pricing outlook for the segment going forward.

A quick update on the progress made across 6 pillars of our Pinnacle Vision:

We launched our Pinnacle journey almost two years back. I’m glad to share that we have made significant progress across all pillars of our Pinnacle journey, leading to the creation of a strong foundation for future growth. Let me share a few highlights:

1) Across businesses, we delivered strong volume growth, Nutrition saw highest B3 volumes in eight quarters and steady Choline growth; Acetyls improved volumes and pricing with market share gains in Europe; Specialty Chemicals continued momentum in Pyridine, Fine Chemicals, and CDMO shipments.

2) Driven by our customer centric approach, We now have 100+ opportunities with Rs.3,400 crore potential. With 20+ confirmed molecules (~Rs.1,500 crore) and an additional pipeline of 10+ advanced stage molecules with Rs.1100 crore peak revenue.

3) From an Operations and ESG perspective, We achieved Rs.120+ crore lean savings and glad to share that we achieved 97th percentile in S&P Global CSA ranking. We also successfully commissioned Bharuch CDMO plant in record 14 months reflecting strong execution. WEF Lighthouse Award and successful USFDA audit of our Bharuch site are testament to the world-class infrastructure we are creating at our plants

4) From a people and organization perspective, we strengthened leadership with key senior hires in Supply Chain, Manufacturing HR, and Design & Tech, and also transitioned to a verticalized structure to drive focused growth across Nutrition, Pharma, Agro, Cosmetics, Industrial, and Semicon segments. We invested heavily in our R&D and Technical teams in last two years.

5) From an awards and recognition perspective, we were certified as a Great Place to Work and ranked among the Top 50 in Manufacturing in India. We were also recognized with the Golden Peacock Award and a British Safety Council distinction.

6) On the M&A front, we completed the acquisition of Remidex Pharma to strengthen our Human Nutrition Premixes portfolio.

The early results from these initiatives have already started to show in our financial results, e.g.

33%+ growth in our EBITDA in last two years, despite tough market demand and declining prices; our Q4FY26 run rate EBITDA is 70%+ higher than Q4FY24 EBITDA, signaling the pace of improvement we could showcase in last two years

Portfolio mix moving in favor of Specialty Chemicals and Nutrition, contributing 85%+ of overall EBITDA; Specialty Chemicals EBITDA almost doubling in last two years

Improved Net Working Capital at 59 days leading to more efficient balance sheet and a Net Debt/EBITDA level of 0.99x

This strong foundation and the early results give us the confidence that our Pinnacle strategy is working well. FY27 is a pivotal year in this journey where we are hoping to accelerate our growth, starting with Q1FY27 itself.”

Q4’FY26 Highlights | Segment Wise Analysis

A. Specialty Chemicals

1. All figures are in Rs Crore unless otherwise stated

2. Before adjustment of Unallocated corporate expense/Income

BUSINESS WISE UPDATES

P&P

- Strong volume momentum in Pyridine & Picolines

- Pricing remained muted with pressure from China continuing; some improvement towards end of quarter

Fine Chemicals

-Pyridine/ Diketene Derivatives: Volume growth across products with pricing remained muted

- Cosmetics: Expanded portfolio beyond Niacinamide; Products under qualification with customers

- Industrial: Volume growth across existing customers;

New customers added in pipeline

CDMO

- Agro: Commenced dispatches of Big CDMO order

- Pharma: Grew our pipeline by 3x+ in last 2 years with innovators and Tier-1 CDMOs

- Semicon: Building R&D lab at Greater Noida with clean room; Increase in funnel across key applications

Business Drivers

- Segment revenue improved, driven by volume recovery across segments, with Fine and Agro Chemicals leading the overall growth

- EBITDA improved significantly due to higher share of value-added CDMO products and Improved contribution from Fine Chemicals

B. Nutrition & Health Solutions

1. All figures are in Rs Crore unless otherwise stated

2. Before adjustment of Unallocated corporate expense/Income

BUSINESS WISE UPDATES

Human Nutrition

- B3: Steady YoY growth in food and cosmetic volumes, with some

softness in pricing across food; cosmetic pricing remained stable

- CC/CBT: Gaining traction with customers in EU/US; steady volume scale up in India

- Premixes: Traction with tier-1 customers in India with acquisition of Remidex Pharma

Animal Nutrition

- B3: Achieved highest volumes in the past eight quarters; Improvement in pricing, driven by strong demand recovery towards second half of quarter

- Choline: Increase in volumes with imports easing from China both on a YoY and QoQ basis;

Improving traction in the EU, with rising volumes following anti-dumping duties on China

- Premixes: Volume growth in domestic market; pricing remained stable

Business Drivers

- Revenue growth driven by strong double-digit volume expansion both QoQ & YoY, led by Niacinamide (Vitamin B3), with favorable mix improvement in Choline

- Margins improved QoQ, supported by a favorable volumes shift in mix toward higher-value end-uses, with increased contribution from Cosmetics and Food segments

C. Chemical Intermediates Segment

1. All figures are in Rs Crore unless otherwise stated

2. Before adjustment of Unallocated corporate expense/Income

BUSINESS WISE UPDATES

Acetic Anhydride

- Overall Volume growth supported by resilient Pharma demand in India and increased market share in Europe; retained market share in India merchant market

- Acetic Anhydride volumes grew strongly YoY, with stable QoQ performance

- Sharp increase in Acetic Acid prices due to disruptions in the Middle East

Ethyl Acetate

- Double-digit growth in Ethyl Acetate volumes on both QoQ and YoY basis

- Prices improved, driven by higher raw material costs, driven by ME disruptions

Business Drivers

- Revenue increased on both QoQ and YoY basis, driven by overall volume growth and improved realizations, supported by higher input costs amid Middle East–led crude inflation

- EBITDA growth driven by higher volumes and better realizations, supported by

pass-through of increased raw material costs

3. Income Statement – Q4’FY26

All figures are in Rs Crore unless otherwise stated

4. Segment P&L – Q4’FY26

All figures are in Rs Crore unless otherwise stated

5. Debt Position as on 31st March, 2026

All figures are in Rs Crore unless otherwise stated

Capex cash outflow for the quarter stood at ?69 crore, primarily went towards commissioning of CDMO plant at Bharuch and ground breaking of new MMP at Gajraula.

Compared to Q3’FY26, the Net debt increased marginally due to higher working capital requirements

The working capital to revenue reduced to 16%, compared to 18% during Q4’FY25.

About Jubilant Ingrevia Limited

Jubilant Ingrevia Limited is a leading player in Specialty Chemicals & CDMO globally, serving Pharmaceutical, Nutrition, Agrochemical, Consumer, Semiconductor and Industrial customers. It offers customised solutions that are innovative, cost effective and conform to global quality standards and has a broad portfolio of 130+ products.

It has over 45 years of legacy in the chemicals industry and is amongst the top players globally in Pyridine & Picolines, Pyridine derivatives, Acetic Anhydride, Vitamin-B3 and many other products. Jubilant Ingrevia Limited has a fast-growing Custom Development and Manufacturing business (CDMO) serving pharmaceuticals, agrochemicals and semiconductor sectors. The Company serves customers in US, EU, Japan, Middle East, South East Asia and other geographies, in addition to domestic market from its 50+ plants across 5 manufacturing facilities in India with a workforce of over 2,300 employees. Its three R&D centres employ 150 scientists working on cutting-edge research and innovation.

Jubilant Ingrevia Limited is a Responsible Care certified company and ranked highly in global ESG indices such as Ecovadis and Dow Jones Sustainability Index. In 2024, Jubilant Ingrevia Limited was also recognised by the World Economic Forum (WEF) and entered its prestigious Global Lighthouse Network (GLN) for deployment of 4IR technologies.

For more information, please visit: www.jubilantingrevia.com.

For more information, please contact:

Earnings Call details: T The company will host earnings call at 5.00 PM IST on 26th May, 2026

Disclaimer:

Statements in this document relating to future status, events, or circumstances, including but not limited to statements about plans and objectives, the progress and results of research and development, potential product characteristics and uses, product sales potential and target dates for product launch are forward looking statements based on estimates and the anticipated effects of future events on current and developing circumstances. Such statements are subject to numerous risks and uncertainties and are not necessarily predictive of future results. Actual results may differ materially from those anticipated in the forward-looking statements. Jubilant Ingrevia Limited may, from time to time, make additional written and oral forward looking statements, including statements contained in the company’s filings with the regulatory bodies and our reports to shareholders. The company assumes no obligation to update forward-looking statements to reflect actual results, changed assumptions or other factors.